Humanoid Robotics: The real challenge is no longer the technology, but scaling up

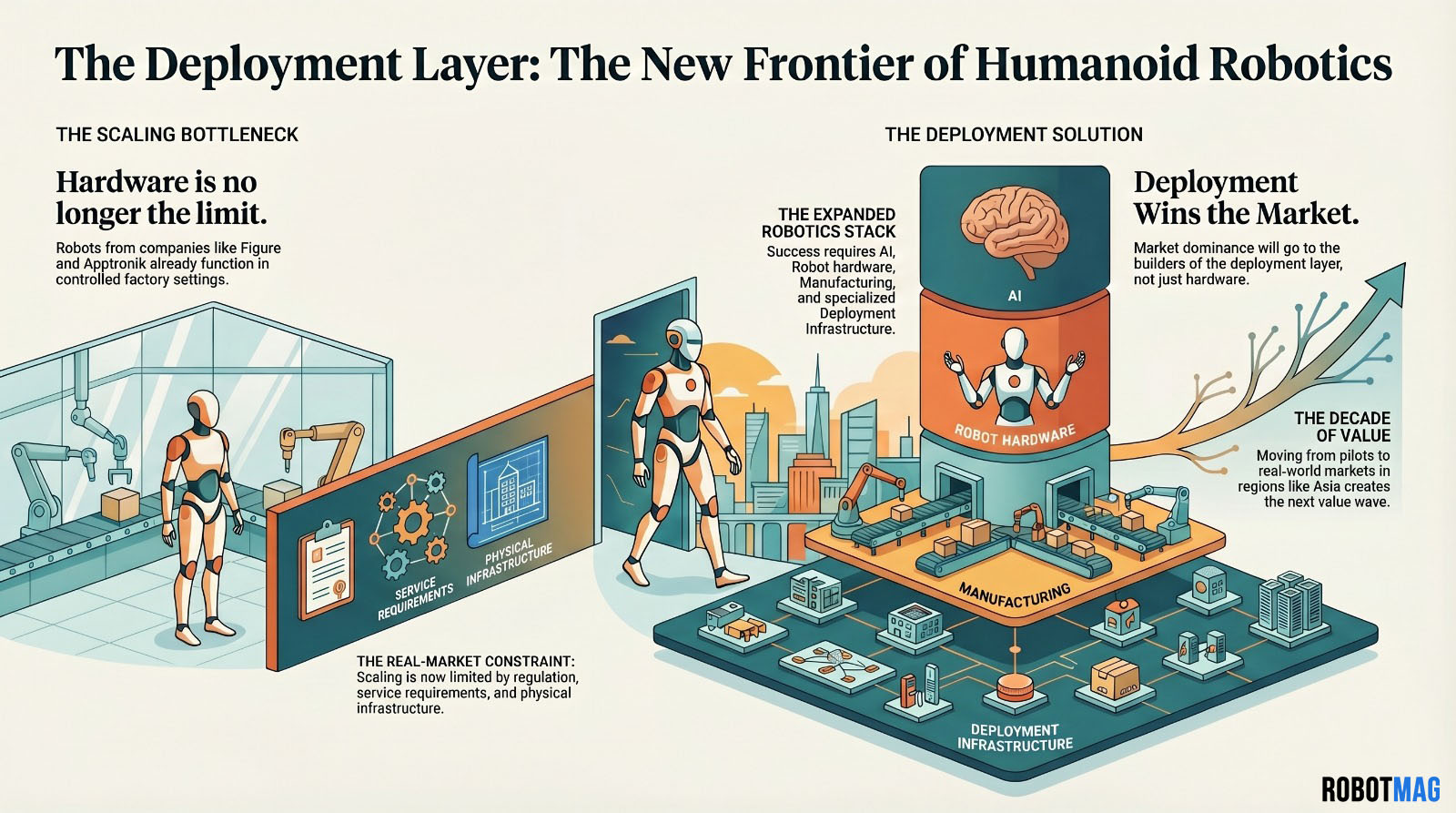

For years, humanoid robotics was seen as a purely technological challenge. Designing machines capable of walking, handling objects, or interacting with their environment was at the heart of innovation. In 2026, that paradigm has changed profoundly. The real bottleneck in the market no longer lies in robots’ mechanical or software capabilities, but in their large-scale deployment.

According to several industry estimates, the global humanoid robot market could reach between $30 billion and $60 billion by 2035, with annual growth exceeding 35%. Yet today, less than 1% of industrial companies use humanoids in real production environments. The gap between potential and adoption is telling.

From Technical Demonstration to Industrial Reality

Recent advances in robotics, driven by artificial intelligence and imitation learning, have made it possible to cross a major threshold. In 2025, several prototypes capable of performing picking or assembly tasks were unveiled. In 2026, some manufacturers are announcing tests involving fleets of 10 to 100 robots in controlled environments.

But those figures remain marginal. For comparison, a single automotive plant can deploy more than 1,000 traditional industrial robots.

The transition toward mass adoption involves challenges of a completely different nature:

- System standardization

- Large-scale maintenance

- Software interoperability

- Total cost of ownership (TCO)

Today, the cost of a humanoid robot still ranges between $50,000 and $150,000, which significantly limits large-scale deployment.

The real challenge is no longer

making a robot walk, but making

it work at scale.

Infrastructure: The New Battleground

Scaling up requires a complete rethink of the infrastructure surrounding humanoid robots. Unlike conventional industrial robots, these machines must operate in unstructured human environments.

This implies:

- Ultra-reliable networks (5G / edge computing)

- Latency below 10 milliseconds for certain critical applications

- Real-time data processing capacity (several gigabytes per hour per robot)

According to a recent study, more than 70% of companies believe their current infrastructure is not ready to accommodate autonomous robots at scale.

Regulation: A Constraint, but Also a Lever

In 2025, several regions, particularly in Europe, began structuring regulatory frameworks around AI and robotics. These regulations impose:

- Strict safety certifications

- Traceability of algorithmic decisions

- Data protection obligations

In sectors such as healthcare, certification timelines can reach 24 to 36 months, significantly slowing large-scale deployment.

However, by the 2028–2030 horizon, harmonized standards could accelerate adoption by creating a trusted framework for manufacturers.

From Hardware to the Service Layer

Historically, robotics was built around hardware. But since 2022, the market has been shifting toward service-oriented models.

The Robot-as-a-Service (RaaS) market is growing rapidly, at an estimated rate of more than 20% per year. Under this model, companies no longer pay for a robot upfront, but for its usage:

- Average monthly cost: $2,000 to $5,000 per robot

- Maintenance included in most offers

- Continuous software updates

This approach reduces entry barriers and enables more gradual adoption.

Industrialization and Supply Chain: The Great Overlooked Issues

Producing a few dozen robots is one thing. Producing thousands is another.

By 2030, some players are targeting production capacities of 10,000 to 100,000 units per year. That requires:

- Securing critical components (semiconductors, sensors)

- Reducing production costs by 30% to 50%

- Standardizing parts

Today, more than 60% of the cost of a humanoid robot is tied to its electronic components.

Market Integration: The Last Mile

Even if the technology is ready, one final obstacle remains: integration into real markets.

The first significant deployments are expected between 2026 and 2030, particularly in:

- Logistics

- Automated retail

- Industrial assistance

Logistics alone could account for up to 40% of humanoid robot use cases by 2030, due to pressure on supply chains and labor shortages.

We are no longer selling machines,

but ecosystems where hardware is

only the visible part of the data layer.

A Redefinition of the Robotics Model

The traditional robotics framework is evolving toward a systemic approach. In 2026, the most advanced players are no longer selling robots alone, but complete solutions integrating:

- Hardware

- Software

- Infrastructure

- Services

- Data

There is a clear convergence with SaaS models, where value shifts toward operations and data management.

Humanoid robotics is entering a new phase. After the era of technological innovation (2015–2025), the decade 2025–2035 will be defined by large-scale deployment.

The bottleneck has shifted toward infrastructure, regulation, and market integration. The companies that will dominate this market will not simply be those designing the most advanced robots, but those capable of deploying them at scale in real-world environments.

The next revolution will not be technological. It will be operational.

FAQ – The Challenges of Industrial-Scale Deployment

2. What is the current gap between the market's economic potential and its actual adoption?

Although the global market could reach 30 to 60 billion dollars by 2035, less than 1% of industrial companies currently use humanoids. This delay is explained by the complexity of moving from tests on small fleets of 10 robots to massive deployments comparable to the thousands of traditional industrial robots already in place.

3. What are the financial and structural obstacles to the massive deployment of these robots?

The unit cost of a humanoid robot, ranging between 50,000 and 150,000 dollars, remains a major hurdle for many companies. Added to this are challenges of standardization, software interoperability between different brands, and the need to establish industrial maintenance capable of managing large fleets.

4. Why has network infrastructure become the new "sinews of war"?

Unlike fixed robots, humanoids move through unstructured environments and require ultra-reliable networks like 5G to ensure latency of less than 10 milliseconds. Processing several gigabytes of data per hour per robot requires a cutting-edge infrastructure that 70% of companies claim they do not yet possess.

5. How does the "Robot-as-a-Service" (RaaS) model transform access to this technology?

The RaaS model allows companies to lease robots rather than buy them, with an average monthly cost between 2,000 and 5,000 dollars. This approach generally includes maintenance and continuous software updates, significantly lowering financial barriers to entry and facilitating gradual adoption by industrialists.

6. What role does regulation play in the speed of adopting humanoid robotics?

The implementation of strict regulatory frameworks, particularly in Europe, imposes rigorous safety certifications and algorithmic traceability. While these standards create a necessary climate of trust in the long term, they can slow down immediate deployment, with certification times reaching up to 36 months in sensitive sectors like healthcare.

7. Which sectors will be the first to massively integrate humanoid robots by 2030?

Logistics is expected to represent about 40% of use cases by 2030 due to heavy pressure on supply chains and labor shortages. Automated retail and industrial assistance are also priority sectors where complete solutions integrating hardware, software, and data will provide immediate operational value.

Stay ahead in robotics, humanoids, and the industry of the future.

Enter your email to access the essentials.